Insights and Strategies

Favouring a Defensive Game for the Second Half

As we officially kick off the second half of 2023, we are still waiting for the long anticipated recession to appear. While we watch interest rates, economic data and inflation measures to see indicators of recession impacting the general economy, the stock market looks ahead to economic growth beyond the (possible) recession. Sometimes, however, the stock market gets a little too exuberant, and although generally focused on the longer term, the market can still be surprised in the short term.

This brings us to our message this month: Regardless of whether Canada (and/or the U.S.) officially dips into recession, we are cautious about short-term negative surprises and volatility in the markets. Now, trying to time the market is a challenging game at best, and staying invested over the longer term is generally a much better strategy, especially through a well-crafted plan suited to an investor’s personal objectives and risk tolerances. Staying invested also helps to avoid missing the most rewarding gains through the business cycle, which generally occur early on in the cycle, as market timers that have stepped out of the market debate whether or not to step back in.

We are also optimistic about longer-term growth opportunities that might be spurred on by factors like the U.S. Inflation Reduction Act, Artificial Intelligence (AI), or an industrial resurgence in North America, as governments look to build manufacturing capacity to protect against future supply chain issues like the ones we experienced through the pandemic. With all that being said, the question is: Are there ‘safe’ sectors to favour during periods of market volatility and general pullbacks in the market? Looking back over 20+ years we can identify sectors that are likely to fare better than others, while allowing investors to remain invested.

Recession: To Be, or Not to Be

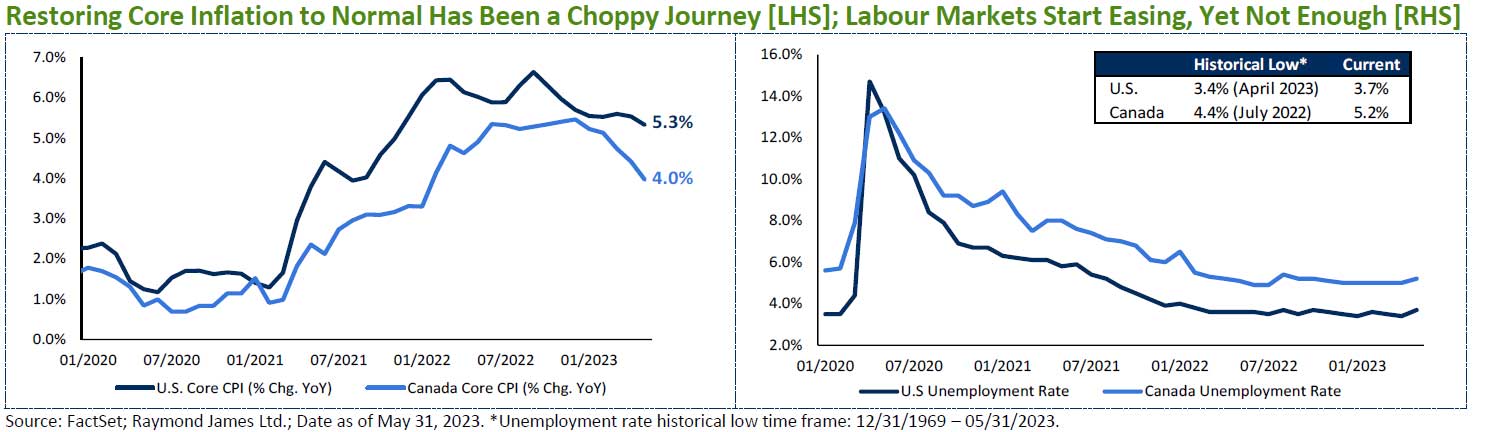

Just before we look at our second-half investment strategy, it’s worth reviewing where the economy is currently sitting. In Canada, we saw still positive Gross Domestic Product (GDP) growth, increasing slightly from 2.1 per cent in 4Q22 to 2.2 per cent in 1Q23. April GDP was flat, but May has been estimated as being up another 0.4 per cent from April. It looks like Canada might skirt recession territory as the consensus is for growth to weaken, but remain slightly above zero per cent from 2H23 into 1Q24, before picking up again through 2H24. While in the U.S. the consensus is for a mild recession, but with an ever-shifting start date, now generally considered to be most likely in 4Q23.

![]()